Investing during COVID-19: The Long and Short of It

Siddhartha Rastogi explores the impact of COVID-19 on investment decisions of HNIs, FIIs, AMCs and retail investors. He also suggests how retail investors can look at investing during COVID keeping in mind the long-term prospects of the economy.

An investment professional with over 2 decades of experience in the capital markets and wealth management, Siddhartha was a founding member of IIFL Wealth and has worked with HSBC, Citibank & UTI bank in wealth management & merchant banking roles. An avid writer on topics of finance, he has also authored a book – 8 Minute Decision.

The interaction of economic principles with the financial markets – along with all of its participants – is complex. And in a dynamic world like ours, ever-changing. The advent of the novel coronavirus has only added on to the complexity, with the future being more uncertain than ever. Times like these are stressful, but for an investor, it could be full of opportunities. In my previous article about the impact of COVID-19 on the economy, I’ve shared my thoughts on what will be the new normal for business.

This piece is going to give you an account of how the current times have affected the capital markets. It will also explore how High Networth Individuals (HNIs), Foreign Institutional Investors (FIIs), Mutual Funds, Asset Management Companies (AMCs), and retail investors, might behave during these unprecedented times. Finally, I’ll share my thoughts on how to approach investing in a time of uncertainty and upheaval in the old way of doing business.

In order to navigate through the capital markets successfully, it is important to employ a strategy that has proven to be consistent over long periods of time. While I’ll elaborate on the distinct characteristics of a business to look out for, I’ve always preferred companies which are ‘Clean and Consistent’.

‘Clean’ businesses are those that flourish because of their inherent DNA. These are businesses that have no political inclination, no political or external influence, and work towards maximizing shareholder wealth. They do not resort to any unscrupulous activities and conduct business based on strong principles.

While the word is self-explanatory, it was rightly said – “Consistency is Key“. I look for businesses that have been consistent with their performance over long periods of time. Typically, consistent businesses are market leaders in their respective industries – they have little to no leverage, an extensive distribution channel, a strong brand, and are consumer-centric. These businesses are focussed in their industry – which is to say that they refrain from entering different unrelated sectors where their know-how can be questioned. That being said, a firm’s consistency is best reflected in its financial statements. The sole purpose of a business is to be profitable and grow their profits at a decent rate over the years. Most shareholders will be willing to own a part of those businesses which add value to their portfolio.

Red flags to watch for when picking companies to invest

While financial statements are the best way to understand a company’s performance, there’s always more to it than what meets the eye. A lot of businesses tweak their financial statements just to paint a rosy picture for its shareholders – inflating sales figures by claiming to have sold goods on credit, paying their auditors higher fees so that they do not unearth the fallacies within the accounting books, frequently changing depreciation methods depending on which method maximizes their profits (artificially). These are a few ways some businesses try to keep the true state of their operations away from the eyes of its shareholders.

Focus, for any business, should be key. Many businesses, instead of reinvesting their profits into their own business, buy shares in different, unrelated firms that have no potential synergies. While it shows that the business does not have confidence in its future strength, it also, often unsuccessfully, tries to penetrate another sector/industry where it does not have expertise. This is one of the reasons why firms that have a very diverse product base (which spans across industries – conglomerates) have not been the best wealth creators for their shareholders.

Investing during COVID: Behaviour of Market Participants

It’s important to understand the behaviour of the different market participants – High Network Individuals (HNIs), Foreign Institution Investors (FIIs), Domestic Institutions Investors (DIIs) such as Asset Management Companies (AMCs) who create and manage mutual fund schemes, as well as retail investors. Their investing behaviour during COVID will affect the stock markets which are often skewed and aren’t the best indicators of the underlying economy. The stock markets may have a strong recovery, not due to the fundamental strength, but due to global liquidity which is available for almost free (as interest rates tend to near zero) as described in my article which analysed of the impact of COVID-19 on the Indian economy.

How will COVID impact decisions of HNIs & FIIs?

Global interest rate levels are very important for determining the behaviour of Foreign Institutional Investors (FIIs) and High Networth Individuals (HNIs). In a world where interest rates are at all-time lows, especially in the developed world, FIIs/HNIs are always on the lookout for investment opportunities which give them more attractive potential returns. What better than emerging market equities? With equity financing given a preference over debt financing, HNIs/FIIs are expected to invest in emerging markets like India. This is expected to drive Indian equities to new highs, and such a large quantum of money flowing into the country will also result in an appreciation in the value of our currency. FII inflows are thus expected to be rampant. HNIs will increase their equity allocation, but they will continue to look at niche assets across businesses and real estate.

Editorial Note: In the chart below, we see that FIIs are currently pulling out money but the trend will reverse in the near future as per the author.

How will Asset Management Companies (AMCs) invest during COVID?

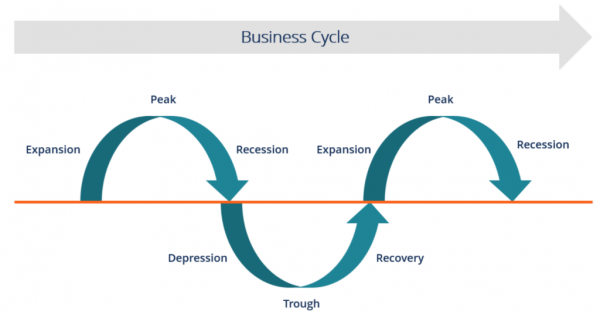

One thing should be clear by now – the global economy is dynamic. Historically, we’d see that an average business/economic cycle lasted for about 8-10 years.

Source: Corporate Finance Institute

Started extensively in the 21st century, modern monetary policy has taken over as one of the key policy tools that central banks use in order to contain any sort of economic malaise. Such policies include cutting down interest rates (to make borrowing money cheaper), increasing the money supply by printing currency, reducing regulatory requirements given to banks by the central bank. These tools, while very effective, are disruptive in nature. Printing money, for example, increases government debt – something the future generations will have to pay for. These tools, in a way, act like steroids which kickstart the economy sooner than otherwise possible. All this, while the underlying strength of the economy remains largely unchanged, or to be honest, deteriorates. Economic indicators (like the GDP) may show that the economy has revived, but this is an artificial escape that governments and central banks create and – surprise surprise – it doesn’t last! They disrupt business cycles in a way that they become shorter – wherein the recovery is fast, but the downfall is faster.

While the hangover from the current global crisis is going to last a long time, it will eventually fade away but will leave behind some permanent changes.

Across asset classes, there will be a jump in short-term and long-term volatility. Economic cycles that lasted for 8-10 years can now be expected to span over 4-6 years. Click To TweetThese monetary policy measures do have consequences in the Asset Management industry as well. Asset managers that rely on making money by entering and exiting a business at the ‘right time’ and those that hope to take advantage of cyclicality in businesses are going to go through hard times as seen previously in 2008 and 2013. To reiterate what I’ve already spoken about, since the adoption of modern monetary policy measures, the behaviour of economic/business cycles have changed. And everyone investing during COVID, including asset managers trying to take advantage of these cycles, will find themselves surprised by how economic cycles behaved differently than they expected.

These disruptions will cause the exit of many prominent asset managers who were trying to do stuff which they think is ‘Out of the Box’.

Quality financial advisory will emerge. Client centricity will be of utmost importance – there will be a culture inculcated wherein clients will pay fees only when they make money. Currently, clients were expected to pay a fixed fee to advisors irrespective of whether the client makes money through the advice or not. That’s set to change, where ‘Winning Together’ is going to be the new norm.

Mutual funds, smallcases, and passive investment products are expected to gain a lot of traction as they will be the most sought after route for retail investors looking to gain exposure to equities. This would also lead to the largest mutual fund managers increasing their fees.

Editorial Note: This guest article is published on the official blog of smallcase Technologies which has created the modern financial product know as smallcases. A smallcase is a basket of stocks/ETFs based on ideas, themes and strategies. They are professionally managed and offer investors more transparency and control over their investments. However, unlike mutual funds, smallcases do not have a fee structure which is a percentage of the corpus; investors pay a fee when they transact.

[cta color=”blue” title=”Discover unique investment ideas” url=”https://www.smallcase.com/discover/explore?utm_source=smalltalk&utm_medium=cta-button&utm_content=article-03&utm_campaign=ttlg” button_text=”Start Exploring”]50+ professionally-managed stock/ETF portfolios[/cta]

Investing during COVID for retail investors

While Mutual Funds, smallcases, and other passive investment vehicles are a retail investor’s best go-to investment methods, a retail investor should add to their portfolio a few names which are available at cheap valuations during this market turmoil. This will help in creating wealth for those investors who have a holding period of 3-5 years.

Here are some of the characteristics and fundamentals one should look at for choosing companies to invest in.

- Dominance: Large companies who have been market leaders in their industry for a while now, and have survived through different market conditions

- Cash-rich: Firms that have liquid cash in the bank can capitalize on investment opportunities

- Negative working capital: This is a situation where the firm’s short-term liabilities (debt) exceeds short-term assets. This is considered as a good sign because it means that the company is effectively funding its growth in sales by borrowing money from its suppliers

- Inelastic demand: Firms dealing in products that have inelastic demand, which means that even though the price of the product might rise, the demand for it will not fall proportionately. This generally happens with essential products like medicines

- B2C businesses: Firms whose customers are the common man instead of other business – FMCG, Pharma are some of the sectors in the B2C space. For more information, here’s an analysis of the Pharma Industry.

In general, it’s best to buy apolitical companies which have gone through several economic cycles and emerged victoriously. Also, it’s advantageous if the promoters of the company have a significant stake in the business – when their skin is in the game, they will work towards maximizing shareholder wealth. Businesses should be focussing on one segment, one vertical and have a single product; specialisation with a large market size.

Before closing out, I’d like to say that for an average retail investor, the advice is simple. Of the total pool of money which you own, allocate a part of it in liquid debt and the rest in shares of high-quality businesses. Survival and general expenses for the next 3 years can be put aside into the debt funds, while the rest can be invested in equity.

Disclaimer: This is a guest article. The views and opinions expressed are those of the author in his personal capacity and do not necessarily reflect the views of smallcase Technologies. None of the opinions in this article should be construed as investment advice.

This article is a part of a new series – Through the Looking Glass. It will explore trending topics in business + finance, the impact of COVID-19 on the Indian economy, and other relevant topics to help you see beyond the news. The series will feature insights from industry leaders, experts, and our editorial team. Want to see a topic, industry or sector covered? Or opinion from an industry leader? Write to justin [at] smallcase.com

[cta color=”blue” title=”Stock Investing made easy” url=”https://smallcase.com?utm_source=smalltalk&utm_medium=cta-button&utm_content=article-03&utm_campaign=ttlg” button_text=”Start Exploring”]1M+ smart investors use smallcases to discover and invest in unique ideas [/cta]

You may want to read

Building a Core Satellite Investment Portfolio

Building a Core Satellite Investment Portfolio

Getting future-ready with Horizon smallcases 🌅🌿

Getting future-ready with Horizon smallcases 🌅🌿

The Electric Vehicle Revolution and the Role of Batteries

The Electric Vehicle Revolution and the Role of Batteries