Paytm’s Plummet: Is This The Apocalypse For Fintech?

India’s first large fintech, the company that got the country’s smallest of tapris to install QR scanners on their stalls is now close to losing its license. The news about RBI’s strict restrictions on Paytm has come as a huge shock to all Indians. After all, “Paytm karna” is synonymous with making online payments for about 10 crore individual users and almost 4 crore merchants using the platform.

There are a lot of questions around this, Is this all about a takeover? Was it the right decision by RBI? and so many more. So, in this newsletter, I am talking about the journey that Paytm has had, restrictions imposed by the central bank on it, whether it is a fair decision, and how this will affect you, me, and our local merchants. And yes I will also discuss the questions mentioned.

The Beginning of Paytm

Once a stall town engineer and now a well-known and highly respected name in the Indian startup and fintech ecosystem, VSS, Vijay Shekhar Sharma set up One 97 Communications in 2000. It took VSS some time to get the financials and operations in place, but then in 2009, Paytm, the digital payments platform as we know it today was launched. The platform launched its payments gateway in 2012, the wallet in 2014, and the Paytm QR in 2015.

However, until then, not many people were using online payment methods. It was only in 2016 that demonetization was announced which in turn pushed the common citizen towards digital payment platforms, and it’s no surprise that Paytm was the market leader then. This was the turning point for Paytm.

I love how moneycontrol has laid down the company’s journey since its inception. Have a look here:

In 2017, the app saw record downloads by over 100 million users. It was the golden era for Paytm as there were still some concerns around UPI, so everyone was keen on using e-wallets, like Paytm wallet. Paytm’s user base started growing, and a plethora of new services and micro apps were introduced making Paytm the only super-app anyone needed.

Towards the end of 2017, Paytm became a payments bank and started its operations as one under the regulation of RBI. It all seemed fine, rather good for the company as India’s then-largest IPO was under process. In 2021, One 97 Communications came up to raise funds for one of India’s largest startups. Paytm’s IPO was revolutionary, it was and is still an inspiration for entrepreneurs.

Have a look at this business snapshot for Paytm by ET Tech for an insight into some numbers:

But wait, if everything has been so nice and shiny, what went wrong? There have been some warnings, actually many warnings. Let’s talk about those!

The Warning Signs 🔴

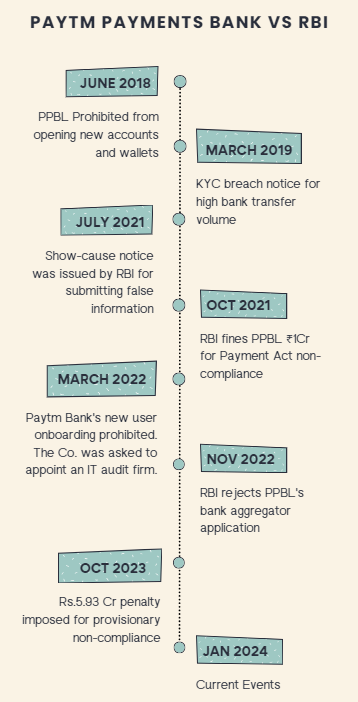

It’s not like we heard of any breaking news around Paytm before January 31, 2024. Well, nothing was evident on the surface, but on the other side, Paytm was receiving multiple warnings from the central bank. Between 2018 and 2023, there were 7 warning signs that preceded the harsh restrictions that we are now talking about.

Have a look at the events when RBI gave Paytm Payments Bank Limited a red signal here:

So now we can safely say that this shot by RBI did not come out of nowhere. There have been reasons, plenty of them. However, the questions I started with still stay relevant.

Is this the story of a hostile takeover or is RBI setting an example?

Everyone’s thinking about whether the butchering of Paytm is a brewing story of a hostile takeover by other market players or if the central bank is just tired of payment banks acting as scheduled banks. Only time will tell the answer to this but for now, business for competitors is booming. PhonePe saw a 45% week-on-week increase in downloads, the BHIM app saw a 21.5% increase, and Google Pay 8.4%. Paytm on the other hand, recorded a 24% drop in the number of downloads.

Is an action this harsh by the central bank fair? Did RBI really need to take such a brutal step against the payments bank?

Everyone has got opinions on the matter, and rather extreme opinions I must add. Most opinions, either speak about the losses that investors and the company are facing or that this move was very much necessary and Payments Banks need to stop acting as Banks. Now there’s merit to both sides but I am concerned about the small merchants who currently use the Paytm wala dabba and the scanner thereof to receive their payments and users who use the platform’s e-wallet, or FASTag recharge facilities.

Here’s what I think. The central bank should have handled the case better.

All that the apex bank of the country has said is that PPBL (Paytm Payments Bank Limited) has been found to be non-compliant with some provisions in the audit conducted. But, we know nothing about the audit or what exactly has come up in the audit report. More information is needed on the reasons behind the actions to give users some clarity.

And then there’s the lack of a contingency plan. There are about 4 crore merchants who use Paytm. They will all be able to withdraw or use whatever funds they have even after 29th February, but is a month really enough for everyone to shift to new payment banks or online payment methods? While you and I will be able to shift to other means, it’s particularly the small merchants like our local tapris, paanwalas, fruit and vegetable vendors, ice cream cart vendors, autowalas, and more who will have to take the real hit. Kyuki aakhir kuch bhi ho, pista toh bechara aam aadmi hi hai na!

P.S.: I’ll miss the sound of Paytm wala dabba every time I make an online payment now. After all, it has become a household voice now.

Explore smallcases by Green Portfolio

Liked this story and want to continue receiving interesting content? Watchlist Green Portfolio’s smallcases to receive exclusive and curated stories!

Green Portfolio is a SEBI Registered (SEBI Registration No. INH100008513) Research Analyst Firm. The research and reports express our opinions which we have based upon generally available public information, field research, inferences and deductions through are due diligence and analytical process. To the best our ability and belief, all information contained here is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable. We make no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results obtained from its use.