If EVs Are the Future, Why Did This Theme Drop 35%?

Windmill Capital was an early mover in the EV space, launching the Electric Mobility Theme smallcase back in late 2017. This theme-based smallcase features companies that are actively investing in the electric vehicle ecosystem and are well-positioned to grow as EV adoption accelerates. The expansion of electric mobility is expected to be driven by a diverse set of players — from two- and four-wheeler manufacturers to oil & gas refiners and chemical producers.

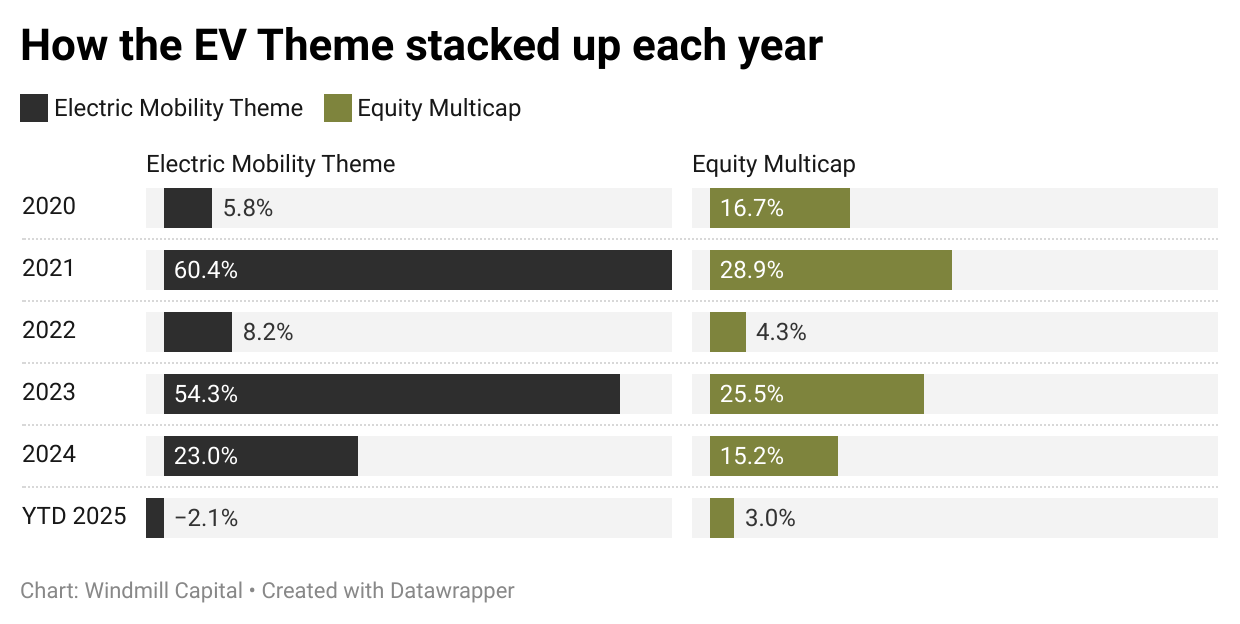

Since early 2019, the smallcase has delivered a compounded annual growth rate (CAGR) of 16.8%, outpacing the broader equity multicap universe, which returned 15.5% over the same period. It has maintained strong and consistent performance, outperforming the comparable index across the 2021–2024 period.

As seen in 2025, performance has been muted, which reflects the nature of the Electric Mobility Theme smallcase—it tends to amplify market movements, often underperforming during sharp downturns but delivering strong outperformance during periods of recovery and growth.

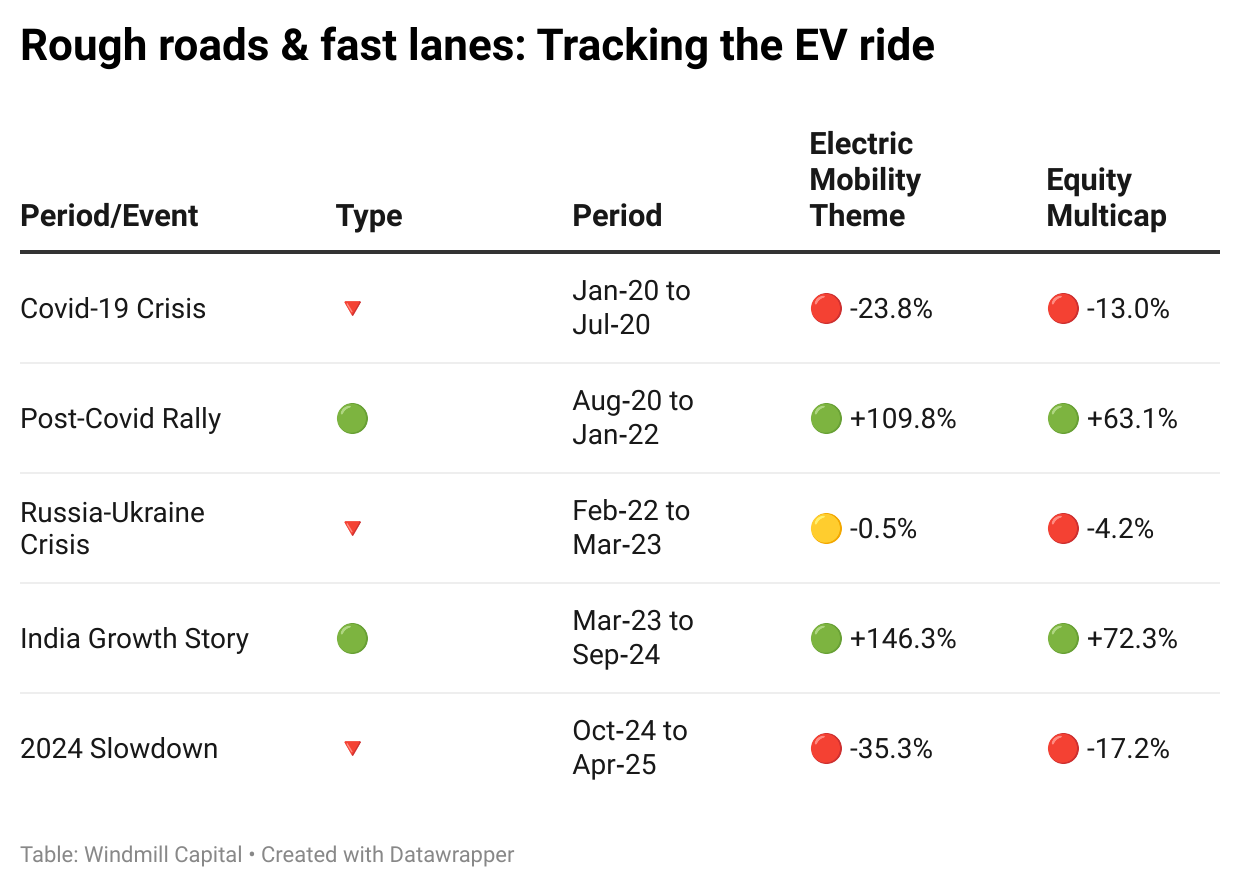

This note analyzes the sharp decline in the Electric Mobility Theme smallcase, focusing on the key factors driving the correction. Specifically, we examine the period from October 2024 to April 2025, during which the smallcase fell by over 35%.

The smallcase comprises a diverse set of companies—including OEMs, auto component manufacturers, charging infrastructure firms, and even an EV software provider. However, a critical aspect to consider is that EV-related revenue still forms a relatively small portion of the overall business for most of these companies.

Take TVS Motor, for instance: despite selling 2.79 lakh electric two-wheelers in FY25 and holding a 21% market share in the EV 2W segment, these accounted for just 6.4% of its total two-wheeler sales for the year. This means that the company’s broader financial performance—driven by its core ICE vehicle business and exports—continues to play a more dominant role in influencing stock prices.

Therefore, it’s essential to evaluate the overall fundamentals of each company rather than focusing solely on their EV contribution when assessing the performance of the smallcase.

Please note that TVS Motors and UNO Minda have been excluded from this analysis, as they were added to the smallcase only in March 2025.

Company-wise Breakdown: EV Manufacturers

1️⃣ Mahindra & Mahindra (M&M)

🔻 Stock decline: 21.3% between 1st Oct ’24 – 7th April ‘25

📈 Mutual fund holding: ↑ from 14.57% in Sept’24 to 16.27% in March ‘25

| Segment | ✅ What Went Well | ⚠️ What Didn’t Work |

| ICE (Auto + Farm Equipment Service) | Strong volume growth (Q2: +7%, Q3: +18%, Q4: +15.3%), healthy ASPs, successful new launches (Thar Roxx, XUV 3XO), upgraded FES guidance to 6–7% | Minor EPS miss in Q3 led to ~10% correction despite strong delivery |

| EVs | Became e-SUV (37.2%) and e-PV (33.1%) segment leader in Q4; launched BE 6e and XEV 9e; clear roadmap with 5 EV SUVs by 2030; EVs EBITDA-positive (standalone) from Q3; Cost optimization and localization underway | Software and manpower delays in Q3 impacted early ramp-up; PLI benefits still pending |

Operationally solid across all fronts. The stock correction appears disconnected from fundamentals, likely driven by sentiment concerns.

2️⃣ Hero MotoCorp (HMCL)

🔻 Stock decline: 38.66% between 1st Oct ’24 – 7th April ‘25

📈 Mutual fund holding: ↑ from 12.92% in Sept’24 to 15.37% in March ‘25

| Segment | ✅ What Went Well | ⚠️ What Didn’t Work |

| ICE (Domestic) | Record festive sales (1.6 mn units), Q3 retail share rose to 32.8% | Motorcycle share fell to 42.3% & scooter share dropped to 6.1% in Q3; overall market share declined to 28.4% in Q4 |

| Exports | FY25 exports grew 43% YoY (2× industry), strong traction in Mexico, Colombia, Nepal | Minor weakness in Turkey and Nigeria |

| EVs | EV market share improved to 7% in Q4; strong Vida presence in 60 towns; launched Vida V2; 2 affordable models lined up for July 2025; PLI application submitted | EV segment not yet profitable; scale-up slower than peers; break-even still 1–2 years away |

Strong export momentum and festive recovery weren’t enough to offset concerns over domestic ICE share loss and limited near-term EV profitability.

3️⃣ Bajaj Auto

🔻 Stock decline: ~40% between 1st Oct ’24 – 7th April ‘25

📈 Mutual fund holding: ↑ from 5.34% in Sept’24 to 6.54% in March ‘25

| Segment | ✅ What Went Well | ⚠️ What Didn’t Work |

| ICE (Domestic) | Strong performance in 125cc+ until Q3; 6 new Pulsar variants in Q4; Freedom CNG push | Lost share in 100cc and 125cc+ segments; FY25 125cc+ share fell from 26% to 24% |

| Exports | FY25 exports +20% YoY; Bajaj outperformed in key EMs (+31%); Brazil ramp-up underway; CNKD plant added capacity | Persisting macro risks in Nigeria, Egypt, and Argentina |

| EVs | Became 2W EV market leader with 25% Chetak share in Q4; launched 35-series electric 2W’s; EVs contributed ~20% to revenue; EV EBITDA turned positive from Q3; PLI benefits already accrued | Early margin drag from Chetak; supply chain uncertainty due to China’s rare-earth metal export restrictions could impact Q1 FY26 production |

Strong export and EV performance couldn’t offset domestic ICE pressures and weak earnings trend (EPS down 6.5% avg), leading to significant derating.

EV Progress vs Stock Performance: Final Takeaways

- EV scaling is real – All three players made significant market share gains and launched credible product pipelines.

- Yet, price performance reflects investor caution – Probable valuation reset, ICE pressures, margin headwinds, and early-stage execution risks weighed heavier than EV optionality.

- Profit visibility matters – Bajaj and M&M showing EV profitability found partial support; Hero’s lack of near-term breakeven visibility hurt sentiment.

- Exports remain a bright spot – Especially for Hero and Bajaj, but not sufficient to override domestic pressures.

For the first time in FY2025, electric scooter and motorcycle sales crossed the milestone of 11 lakh units in total volume. However, this headline growth masks a concerning trend—EV penetration in the two-wheeler segment remains sluggish. While EVs accounted for 4.9% of domestic two-wheeler sales in FY23, the share has inched up to just 5.9% in FY25.

A major factor behind this stagnation is the reduction in incentives from June 2023, which drove up retail prices. However, the deeper challenge lies in consumer hesitation. Most two-wheeler buyers are highly price-sensitive and cautious with big-ticket purchases. Unlike ICE vehicles, EVs are yet to establish a proven track record for reliability, durability, low maintenance, and resale value. To drive faster adoption, it’s not just competitive pricing—but also building trust in these fundamentals—that will be key.

EV spare parts makers

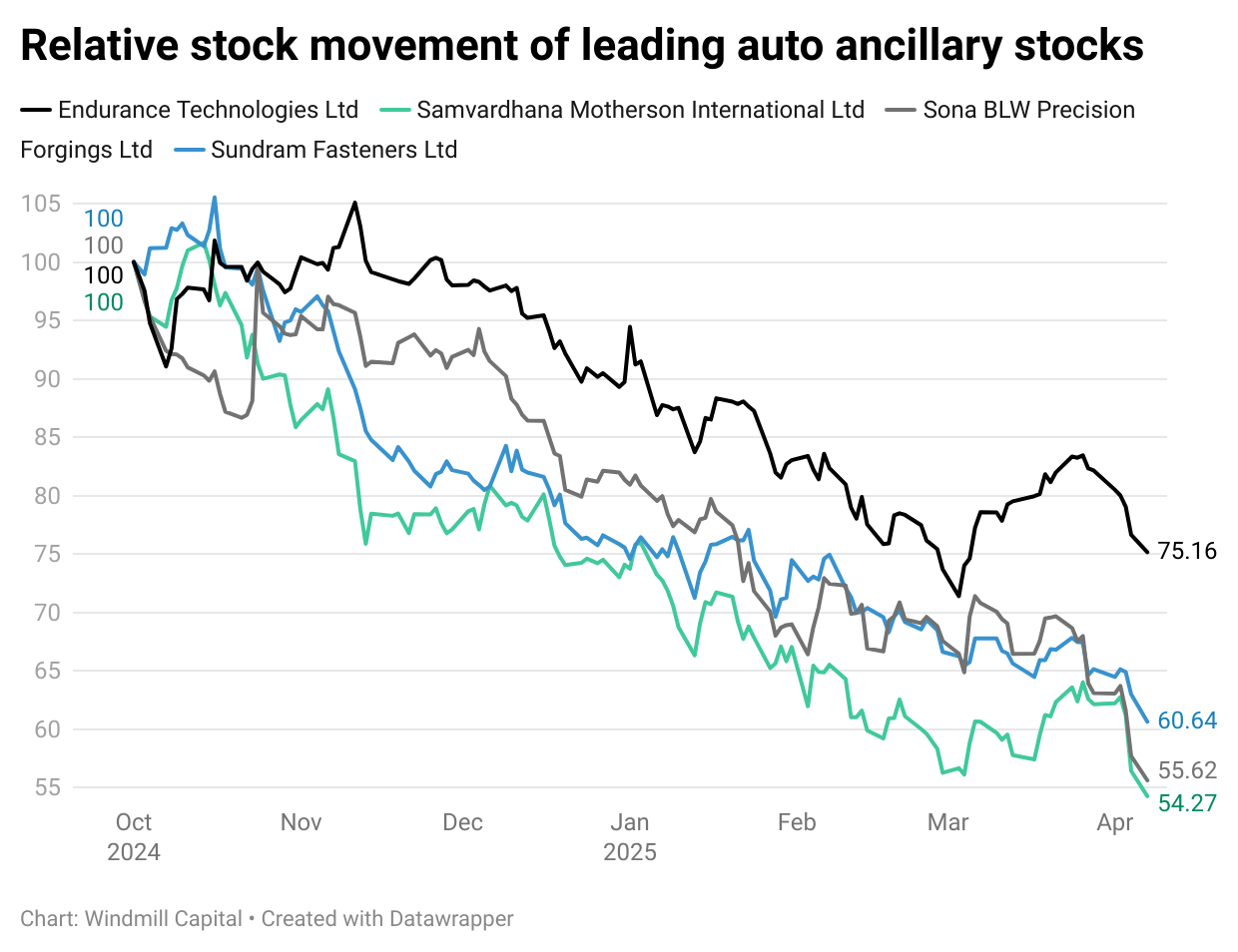

As evident, the four auto ancillary stocks in the basket declined by approximately 25% to 46%.

Between September 2024 and March 2025, the four auto ancillary companies—Sona BLW, Sundram Fasteners, Endurance Technologies, and Samvardhana Motherson—delivered varied performances, with electric vehicle (EV) dynamics playing a central role in shaping outcomes.

Sona BLW maintained a strong EV focus, with EVs contributing 76–78% of its stable ₹23,100–₹24,200 crore order book. EV revenue mix improved from 33% to 39%, supported by 48–53% YoY growth. However, execution challenges, including delayed EV programs and OEM disruptions, led to a Q4 revenue/EBITDA decline of 4%/1%. Still, the company secured ₹4,700 crore in new EV orders during FY25.

Endurance Technologies also saw strong traction in EVs, especially through its Maxwell subsidiary, which achieved EBITDA breakeven in Q4. Of its ₹1,199 crore FY25 order wins, ~37% were EV-related, pushing the cumulative EV order book beyond ₹1,000 crore. Production has begun for ₹1,400 crore worth of EV orders, with another ₹1,000 crore pipeline set for FY26.

Samvardhana Motherson faced margin pressures across segments in Q4, but its total value of confirmed customer orders rose to USD 88 billion (~₹7.3 lakh crore), with EVs forming 24% of the pipeline. While core growth was muted due to global macro and supply chain issues, the EV share in future revenues remains significant.

Sundram Fasteners, in contrast, reported modest growth with limited EV-specific commentary, suggesting a more traditional product mix.

Overall, while operational performance was mixed, EVs remained a clear strategic focus for Sona BLW, Endurance, and Motherson, contributing materially to future order pipelines. Mutual fund holdings remained stable across the board, except for a modest decline in Endurance.

EV charging infrastructure

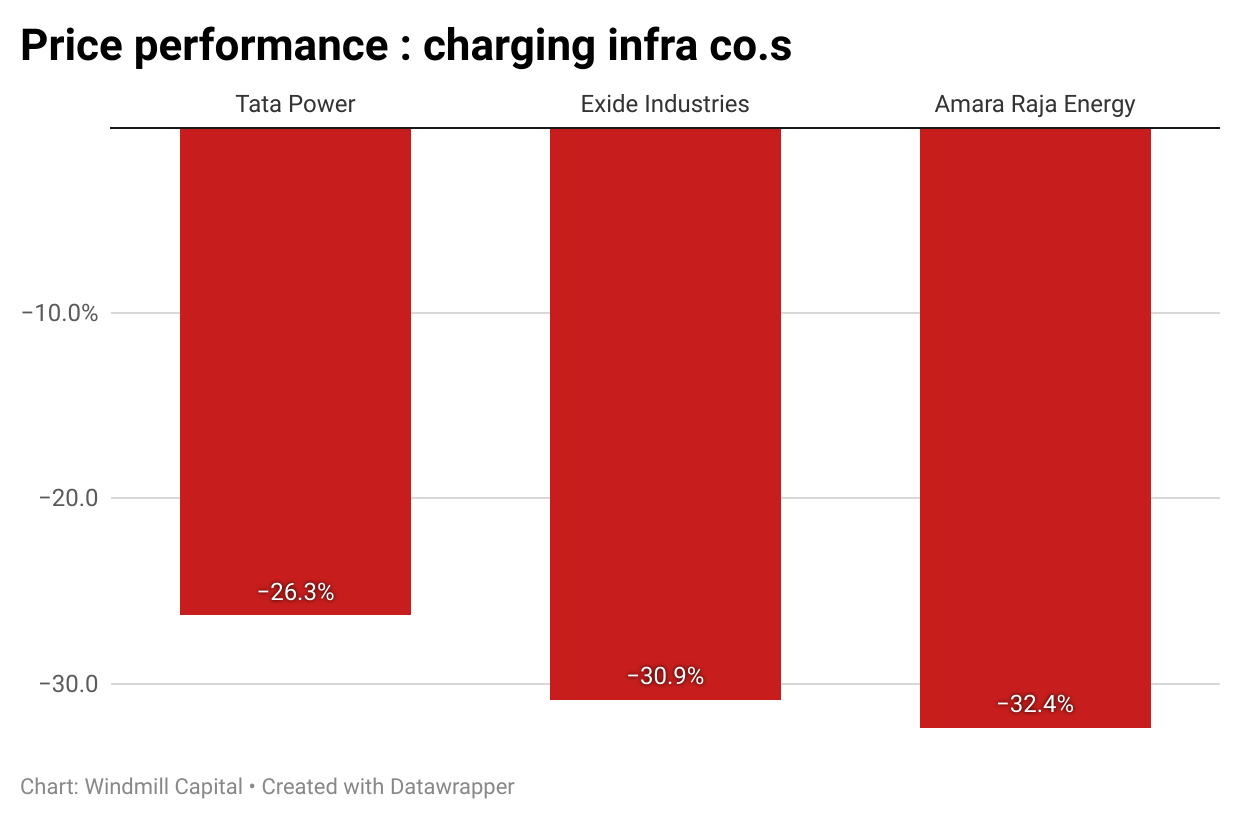

Between September 2024 and March 2025, Exide Industries, Amara Raja Energy & Mobility (ARENM), and Tata Power (TPWR) showcased varied operational and financial outcomes, with significant developments in their EV and energy transition strategies.

Exide continued its aggressive pivot toward EVs by investing ₹36,000 crore into a 6 GWh lithium-ion cell manufacturing plant (NMC + LFP), with trial production set for CY25. It is in advanced discussions with multiple OEMs and aims to be among the first cell producers in India. While core business performance remained steady, OEM demand stayed weak, and margin pressure from higher expenses persisted. Mutual fund holdings declined from 12.59% to 11.11%.

Amara Raja also advanced its EV plans, operating two battery-pack assembly plants (7 GWh capacity) and planning a 16 GWh gigafactory, with Phase 1 (4 GWh) targeted for 1HFY27. It invested ₹850 crore to date in this segment and aims to scale to 8–10 GWh for breakeven. The company faced profitability pressures due to commodity inflation and state-imposed power adjustments, while exports and telecom demand weakened. Mutual fund holdings fell from 6.25% to 5.74%.

Tata Power, meanwhile, made robust strides across clean energy and EV infrastructure. It added 1,026 MW in renewable capacity during FY25, took its operational green capacity to 6.9 GW, and is on track for 9.9 GW more. TP Solar’s cell and module operations ramped up to high utilization, supplying ~3.3 GW in FY25. On the EV front, TPWR installed over 50,000 home chargers and 380 bus charging points. With ₹25,000 crore capex planned for FY26—largely for RE and transmission—the company continues to lead among diversified energy players, and mutual fund holdings have steadily increased.

Exide, Amara Raja, and Tata Power are all ramping up their EV and energy transition efforts, but at varying stages. Tata Power leads with an integrated solar and EV charging network, backed by strong execution and rising institutional interest. Exide has invested heavily in lithium-ion cell manufacturing, aiming to be a first mover, while Amara Raja is cautiously scaling its new energy business amid margin pressures and aggressive global pricing. While Tata Power shows near-term strength, Exide and Amara Raja offer longer-term potential with higher execution risks.

EV Software

Despite a sharp decline in share price during the period, institutional interest in KPIT Tech remained strong, with mutual fund holdings steadily increasing—signaling sustained confidence in its long-term potential.

Operationally, KPIT delivered consistent top-line growth across quarters, supported by a healthy deal pipeline and improved profitability. The company navigated currency headwinds and cautious OEM spending by leveraging operational efficiencies and expanding its offshore delivery capabilities.

Margins improved steadily, aided by cost optimization, better revenue per employee, and a growing share of high-value strategic accounts. Bookings remained strong, particularly in the passenger vehicle segment, with record deal wins in areas like autonomous driving, electric powertrains, and software-defined vehicles.

Geographically, Asia outperformed, while the U.S. and Europe showed some weakness due to protectionist policies and tariff pressures. KPIT responded by focusing on high-growth verticals and improving cash flow, which allowed it to cancel planned equity dilution and fund M&A through internal accruals.

While management held off on providing FY26 guidance due to global demand uncertainty, the company remains structurally well-positioned—backed by a strong balance sheet, a growing share of next-gen mobility solutions, and deepening client relationships.

Conclusion

The future of mobility is being built. It may not move in a straight line—but it’s moving.

The recent correction in the Electric Mobility Theme smallcase—despite strong mutual fund inflows and continued operational progress across components of the EV value chain—highlights the early-stage, high-beta nature of the theme. While EV contributions remain modest in many portfolio companies, long-term fundamentals are strengthening through growing order books, improving profitability in EV segments, and strategic investments in cell manufacturing, software, and charging infrastructure.

This phase is one of transition, not reversal. For long-term investors, staying invested through volatility may be key to capturing the structural upside as EV adoption scales, margins improve, and EV-led revenue becomes more material across companies. Near-term challenges around demand visibility, policy uncertainty, and ICE headwinds may weigh on sentiment, but the broader ecosystem buildout remains intact.

Disclaimer: Investment in securities market are subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, membership of a SEBI recognized supervisory body (if any) and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The content in these posts/articles is for informational and educational purposes only and should not be construed as professional financial advice and nor to be construed as an offer to buy /sell or the solicitation of an offer to buy/sell any security or financial products.Users must make their own investment decisions based on their specific investment objective and financial position and using such independent advisors as they believe necessary. Windmill Capital Team: Windmill Capital Private Limited is a SEBI registered research analyst (Regn. No. INH200007645) based in Bengaluru at No 51 Le Parc Richmonde, Richmond Road, Shanthala Nagar, Bangalore, Karnataka – 560025 creating Thematic & Quantamental curated stock/ETF portfolios. Data analysis is the heart and soul behind our portfolio construction & with 50+ offerings, we have something for everyone. CIN of the company is U74999KA2020PTC132398. For more information and disclosures, visit our disclosures page here.