smallcase in Focus: Speciality Chemicals

Speciality chemicals are specific products providing a wide range of effects on which various industries rely. They are recognised for what they do and the kind of solutions they provide to meet customer application needs. For example, caramel manufactured from sugar is a commercially produced speciality chemical. Caramel colouring is extensively used in the manufacturing of soft drinks and confectionery items.

The speciality chemicals segment comprises a significant portion of India‘s chemical industry. The Indian speciality chemicals industry has expanded exponentially in recent years. It represents 22% of India‘s overall chemicals and petrochemicals market and is valued at $32 bn. The industry is anticipated to reach $64 bn by 2025 at a CAGR of 12.4%. Speciality chemicals account for a significant share of more than 50% of chemical exports.

What is driving the growth of the speciality chemicals industry in India?

- China contributes to 18% of speciality chemical exports globally, which is nearly 4 times the value of Indian exports. Multinational companies have relied on China for its favourable business climate & cheap labour for decades. However, the cost of doing business in China has been increasing recently due to higher labour costs and increased environmental restrictions. These factors alongside supply chain disruptions during covid have forced MNCs to re-evaluate their company strategies in terms of the location of their business activities and manufacturing sites. Lower cost of operations, availability of skilled labour, and favourable Govt policies have allowed India to present itself as a viable alternative market for various industries including speciality chemical companies.

- Rising disposable income, the median age of the population, urbanization etc. have all been fueling demand for speciality chemicals domestically, from end-user industries like pharmaceuticals, food, construction, electronics, dyes and pigments, among others.

- Favourable Govt policies around aspects like setting up a dedicated Petroleum, chemicals and petrochemicals investment region, PLI scheme for chemicals, setting up of vision 2034 blueprint for chemicals sector etc.

While the macro picture is bright, the recent performance of speciality chemical companies on the bourses has not been so great.

| Price performance % 1m | Price performance % 3m | Price performance % 6m | Price performance % 1y | Price performance % 3y * | Price performance % 5y * | ||

| Refinitiv India Specialty Chemicals Index | -3.4% | -13.5% | -15.6% | -14.3% | 15.3% | 19.4% | |

| Nifty 100 | -5.0% | -6.0% | -3.0% | 0.4% | 12.4% | 9.8% | |

| Nifty 500 | -4.6% | -5.4% | -2.6% | 1.3% | 13.9% | 9.7% |

Speciality chemicals – recent performance

During the past year the Refinitiv India Specialty Chemicals index , an index constructed by data provider Refinitv Eikon and that tracks Indian specialty chemicals sector, has dropped by 14.3% compared to flattish performance by Nifty 100 and Nifty 500. However, on a 3-year and 5-year basis, the Speciality Chemicals Index has given handsome returns and comfortably beaten the performance of large-cap and multi-cap indices. To understand what is ailing the speciality chemicals index we analyzed the constituents of the Refinitiv India Specialty Chemicals Index.

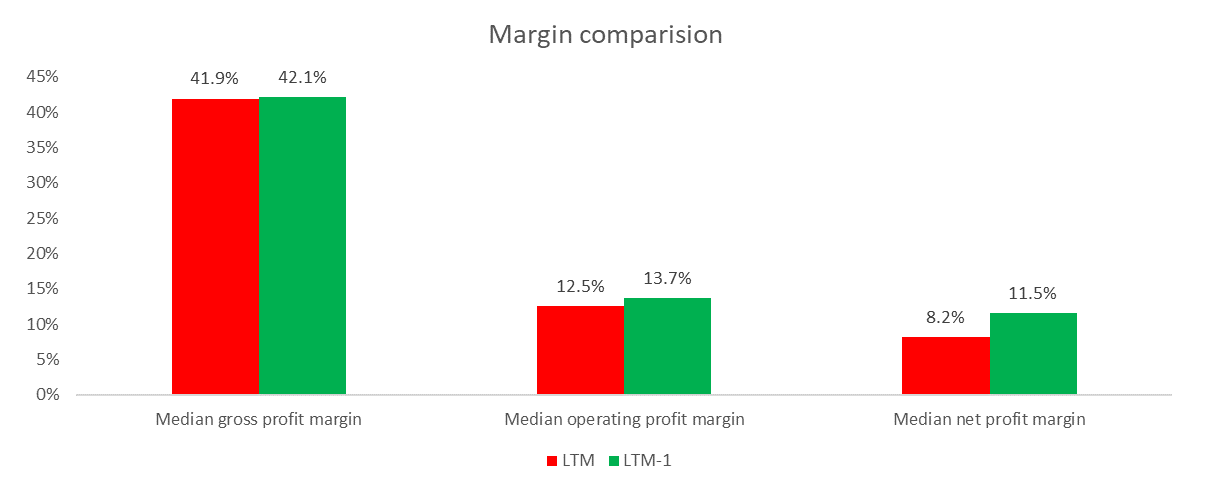

While the topline has been recovering from covid impact and has been growing well, bottom line has seen regrowth.

**LTM-1 : Year ago period compared to LTM

The bottom line has been de-growing because of margin pressure.

Lets deep dive into the performance of a sample list of companies from the Specialty Chemicals smallcase to understand the above phenomenon better.

- Asian Paints

Asian Paints makes and sells paints, coatings, and other products related to home decor.

During the previous 4 quarters, the company has recorded an average revenue growth of 23.3% on a year-on-year basis (YOY). High volume growth as well as price hikes have aided the top-line growth. During the first 9 months of FY23 the company has added ~10,000 new retail points.

However higher raw material prices and an adverse product mix have been affecting the company’s margins. Gross profit margin during the last 4 quarters was 37.6% compared to 40%+ that was recorded during pre covid times. Similarly, the operating margin has dropped to 14.5% from 16-17% levels witnessed during pre covid times. Due to these factors, Asian Paints’ stock price has corrected by ~22% between Aug ‘22 – Feb ‘23.

However, it is not all gloom and doom for the company. According to the company’s management, easing inflationary pressure, increased demand from rural India due to good monsoon season and higher MSP, and renewed interest for industrial paints due to auto sector recovery are all positives. The company has envisaged a capex of Rs.8750 cr over the next 3 years for capacity enhancement, backward integration and acquisitions. During the Dec ‘22 quarter, the company announced an additional capex of Rs.2000 Cr to set up a new water-based manufacturing facility.

- Tatva Chintan Pharma

Tatva Chintan Pharma is engaged in the manufacturing of a variety of chemicals including structure-directing agents (SDAs), phase transfer catalysts (PTCs), electrolyte salts for capacitor batteries, and pharmaceutical and agrochemical intermediates, and other speciality chemicals (PASC). The company’s products find application in automotive, petroleum, pharmaceutical, agrochemicals, paints and coatings, dyes and pigments, personal care and flavours and fragrances industries.

During FY22 period, the company derived 52% revenue from structure directing agents (SDA’s), 23% from phase transfer catalyst (PTC’s), 24% from pharma and agrochemical intermediaries and the balance from others. During the first 9 months of FY23, the SDA segment has only contributed 24% to the topline whereas PTC and pharma segments have contributed 35% each to revenues. Because of this revenue and net profit for 9MFY23 have dropped by ~11% and ~64% respectively compared to the same period the previous year.

The Automobile sector is a major contributor to the company’s SDA segment and the company has been receiving very little business from this sector. The decline of the heavy vehicles industry in China and pressure in Europe has affected the SDA segment. While the segment saw some improvement in Dec ‘22 quarter, full recovery is expected to happen only after the 1st quarter of FY24. The company has also been witnessing margin pressure due to higher commodity, packaging and energy costs.

While the company’s ex-SDA portfolio has recorded good growth, that has not been enough to shore up the stock’s price. Since the company was added to the Specialty Chemicals smallcase in March ‘22, it has been corrected by 12.6%.

- PI Industries Ltd

PI Industries derives 74% of its revenue from custom synthesis manufacturing (CSM) and the remainder from domestic agro chem formulations. Under the CSM segment, the company is involved in target discovery, molecule design, analytical & process development etc. The Company’s agrochemical products categories include insecticides, fungicides and herbicides.

Covid 19 pandemic did not have any impact on the operations or financials of the company. The company was able to maintain its high growth rate as well as margins during the pandemic. During the first 9 months of FY23, the company recorded 26.2% and 48.4% revenue and net profit growth respectively. The company has been able to improve its margins also during this period. Significant revenue growth in the CSM segment driven by higher volumes has contributed to the good performance of the company. In line with the broader market trend, the company’s stock price has been stable since Aug ‘22.

Key takeaways

The pandemic and subsequent macro challenges like high inflation and supply chain disruptions have had varying impacts on different segments of the specialty chemicals industry in the country. While domestic oriented segments like construction chemicals, which includes Asian Paints, have seen recovery in demand, their margins have been impacted due to a spike in raw material prices. Entities like Tatva Chintan Pharma, that have significant external exposure and cater to end user industries like automobiles and textiles, have been significantly impacted due to lower sales and margin pressure. Companies like PI Industries, that deal in agrochemicals, API’s etc, have not been impacted and continue to see positive topline and bottom line growth. While challenges will continue to persist in the near term, long term prospects for the Specialty chemical industry in India continue to be bright.

Disclaimer: Investment in securities market are subject to market risks. Read all the related documents carefully before investing. The content in these posts/articles is for informational and educational purposes only and should not be construed as professional financial advice and nor to be construed as an offer to buy /sell or the solicitation of an offer to buy / sell any security or financial products.

Users must make their own investment decisions based on their specific investment objective and financial position and using such independent advisors as they believe necessary.

Windmill Capital Team

Windmill Capital Private Limited is a SEBI registered research analyst (Regn. No. INH200007645) based in Bengaluru at No 51 Le Parc Richmonde, Richmond Road, Shanthala Nagar, Bangalore, Karnataka – 560025 creating Thematic & Quantamental curated stock/ETF portfolios. Data analysis is the heart and soul behind our portfolio construction & with 50+ offerings, we have something for everyone. For more information and disclosures, visit our disclosures page here –https://windmillcapital.smallcase.com/#disclosures

You may want to read

Strategic Analysis: The Persistent-Nagarro $2.9 Billion AI Consolidation

Strategic Analysis: The Persistent-Nagarro $2.9 Billion AI Consolidation

Why India’s Retail Investors Are Embracing Quant Investing

Why India’s Retail Investors Are Embracing Quant Investing

India’s Great Ethanol Shift: What it Means for Your Portfolio

India’s Great Ethanol Shift: What it Means for Your Portfolio