Homeownership: A Personal and Financial Milestone

One of our PMS clients recently bought two homes, and he resides in the EU. He bought the home with the anticipation that rental yields will remain the same (which it did) and the housing market will continue to grow as it has in the past. And to no surprise, both of these premises turned out to be true. However, what he didn’t anticipate was the rise in interest rates and how that would eat into his pockets.

You may ask, how come home prices witnessed growth despite the rise in rates? Oh yes, it did, because, at the end of the day, it all comes down to supply and demand, economics 101.

Buying a home is a landmark decision in the lives of most people, but with the soaring housing prices in the US, it has become increasingly difficult. Today, we are talking about just that. Let’s see what’s happening in the housing market.

The Soaring Home Prices

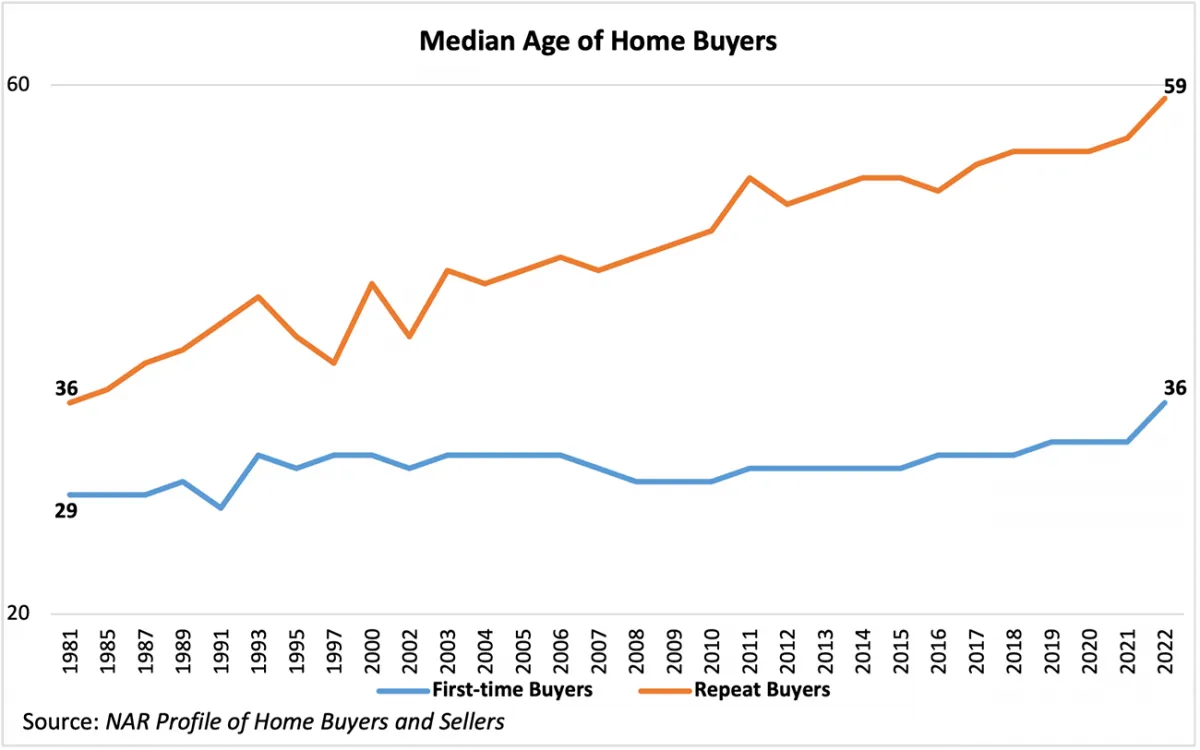

The typical age of a first-time homebuyer in the U.S. has gone from 33 two years ago to an all-new high of 36 now. This suggests many individuals are delaying entering the property market due to steep prices and affordability concerns at this time.

Now while we know the demand-supply economics is the issue, let’s see how it is actually playing out.

- As a result of a decade of insufficient construction, the United States is facing a chronic undersupply of homes. And then there’s high mortgage rates which create a lock-in effect, discouraging homeowners from selling their properties and reducing housing market liquidity. The housing inventory is estimated to be 3-5 million units short of meeting the demand. The scarcity of existing homes in the market worsens the supply-demand imbalance. The result is that home prices have experienced a significant surge of 27% since the end of 2019.

You’d know that while making any investments or expenses, the deciding factor is setting one’s income and savings as the base. Housing takes a major chunk of our incomes, whether it’s rentals or installments. While everyone makes accommodations for this, here’s what’s happening – the share of income required to purchase a home has reached its highest level ever. This means that a larger portion of individuals’ income is now being allocated towards housing costs.

Dive into data: The chart below is an apt depiction of the housing prices reaching all-time highs.

Interest Rates and Mortgages

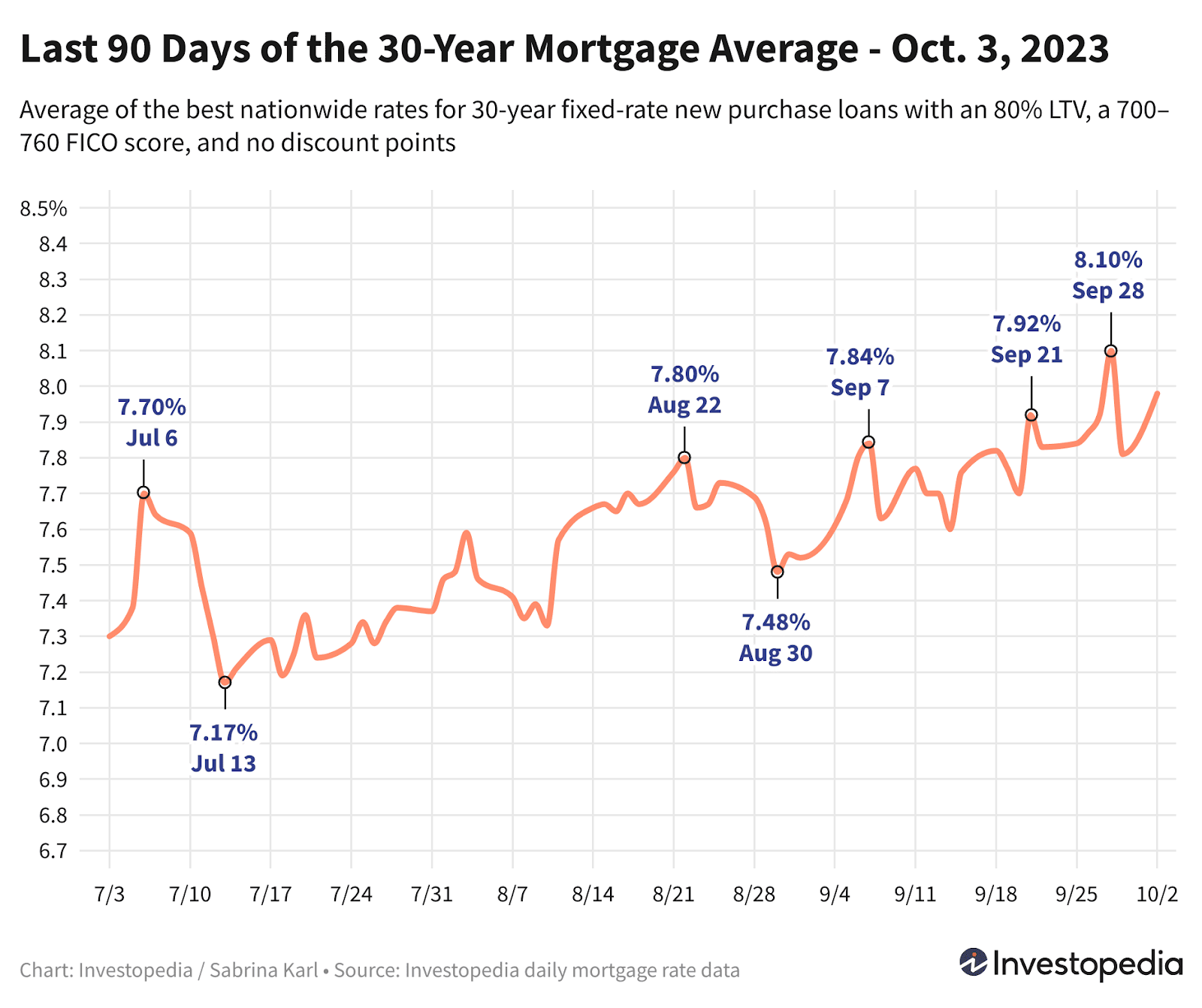

Over 60% of homebuyers rely on loans to finance their home purchases globally. Seldom are savings sufficient to buy a home, and thus we resort to debt. However, with the interest rates hike by the Fed, buyers are now facing challenges due to high-interest rates averaging around 7.83% for 30-year loans.

Now, here’s the thing – the Federal Reserve is in a tricky situation. While higher rates can help rein in rising prices, it also pushes up loan rates for homebuyers. Obviously, no one wants to pay more for a home loan. So, on top of high home values, buyers now have to deal with costlier financing too.

Dive into data: For much of the past decade, rates were historically low as the Fed held rates near zero after the Great Recession. Mortgage rates mirror long-term bond yields, which rise when the Federal Reserve aggressively hikes its short-term interest rate to combat high inflation. This year, the Fed has enacted several three-quarter point rate increases, driving mortgage rates above 8%.

Now even though potential buyers may face expensive financing options, the overall demand for homes remains strong enough to keep prices from decreasing significantly.

Dive into data: The chart below illustrates the steep decline in housing inventory levels nationwide over the past 2 decades.

Outlook for the Future

While it is disappointing for the millennials to see a housing surge, they stay hopeful keeping the demand levels up. And, rightly so there are signs these hurdles may become less steep over time.

Despite the challenges posed by surging home prices and the affordability crisis, there are positive signs in the housing market. With consecutive monthly gains and a 5% increase since February, housing prices are showing a gradual recovery and stability. Strong demand for homes, despite expensive financing, has helped maintain stable prices.

Explore Green Portfolio’s smallcases

Liked this story and want to continue receiving interesting content? Watchlist Green Portfolio’s smallcases to receive exclusive and curated stories!

And for all you Green Portfolio subscribers, we’re rolling out Exclusive Perks!

Use Promocode SCMINT30 on Mint Premium’s 1 Year or 2 Year plan to get 30% OFF on your purchase! Offer Valid until 31st December, 2023.

Green Portfolio is a SEBI Registered (SEBI Registration No. INH100008513) Research Analyst Firm. The research and reports express our opinions which we have based upon generally available public information, field research, inferences and deductions through are due diligence and analytical process. To the best our ability and belief, all information contained here is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable. We make no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results obtained from its use.

You may want to read

Vision 2024: Insights for the New Year with Alok Jain

Complete Guide to the Indian Telecom Sector and Top Telecom Stocks in India

Theme of the Rebalance: Sustainable Efficiency

Vision 2024: Insights for the New Year with Alok Jain

Complete Guide to the Indian Telecom Sector and Top Telecom Stocks in India

Theme of the Rebalance: Sustainable Efficiency

Green Portfolio

Green Portfolio