Optimal Rebalancing Frequency: How Often Should You Rebalance Your Momentum Portfolio?

To unravel the optimal rebalancing frequency for a momentum strategy, we embarked on an experiment that shed light on this critical aspect of investment management. Rebalancing, the periodic adjustment of portfolio allocations, plays a pivotal role in harnessing the potential of momentum investing while mitigating associated risks. Join us as we delve into the findings of our experiment and explore the intricacies of rebalancing in momentum strategies.

Explanation of Momentum Strategy

Momentum investing is grounded in the principle of identifying and exploiting trends in asset prices. This strategy involves buying assets that have exhibited strong recent performance and selling those that have underperformed. The underlying assumption is that assets with positive momentum will continue to perform well in the near future, while those with negative momentum will continue to lag.

Importance of Rebalancing

Rebalancing is crucial for several reasons:

- Control Risk: Rebalancing helps maintain the desired level of risk exposure within the portfolio. Without periodic adjustments, the portfolio’s composition may drift significantly, leading to unintended concentrations of risk.

- Preserve Diversification: Rebalancing ensures that the portfolio remains diversified across different asset classes and sectors. This diversification helps mitigate the impact of adverse market movements on overall portfolio performance.

- Capture Gains and Manage Losses: By systematically rebalancing the portfolio, investors can capture gains from outperforming assets and reinvest them into underperforming ones. This disciplined approach allows investors to capitalize on market trends while managing losses effectively.

Factors Influencing Rebalancing Frequency

Several factors influence the optimal frequency for rebalancing:

- Transaction Costs: Frequent rebalancing may incur higher transaction costs, potentially eroding returns over time. Investors must strike a balance between the benefits of rebalancing and the associated costs.

- Tax Considerations: Rebalancing can trigger tax liabilities, particularly in taxable accounts. Investors should carefully consider the tax implications of their rebalancing decisions and plan accordingly.

- Market Volatility: Higher market volatility may necessitate more frequent rebalancing to adapt to changing market conditions and manage risk effectively.

- Investment Goals and Time Horizon: Rebalancing frequency should align with investors’ investment goals and time horizon. Long-term investors may opt for less frequent rebalancing, while short-term traders may prefer more frequent adjustments.

The Experiment: Testing Long-Term Relative Momentum

In our experiment, we sought to explore the effect of rebalancing frequency on the effectiveness of long-term relative momentum within the Indian stock market context. Specifically, we focused on calculating momentum as one-year returns with a one-month lag. It’s crucial to note that our experiment is designed for illustrative purposes and serves as a starting point for understanding the principles of momentum investing.

Methodology

We utilized historical data from the National Stock Exchange (NSE) to construct our momentum strategy. Our approach involved selecting the top 200 stocks listed on the NSE, forming the universe for our experiment. Within this universe, we calculated the one-year returns for each stock with a one-month lag, capturing the momentum effect over a longer-term horizon. We then backtested the strategy for the rebalancing frequencies of one week, one month, one quarter, and one year.

Contrasting Approaches: Wright Research’s Definition of Momentum

It’s important to highlight that our experiment focuses on long-term relative momentum, which differs from other definitions of momentum, such as those employed by Wright Research. While Wright Research may utilize alternative methodologies and timeframes to identify momentum opportunities, this blog just offers a simplified illustration of momentum principles within the context of the Indian stock market.

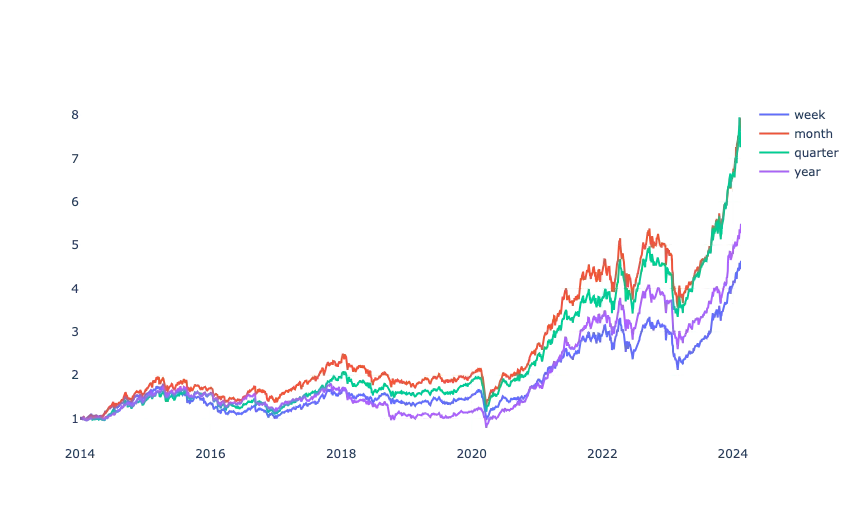

Showcase of Results

Let’s take a look at the performance metrics of a momentum strategy over different time horizons:

| Week | Month | Quarter | Year | Nifty | |

| CAGR | 16.6 | 23.0 | 22.5 | 18.6 | 14.4 |

| Volatility | 23.0 | 22.9 | 22.8 | 23.3 | 15.1 |

| Max Drawdown | 45.7 | 48.5 | 44.3 | 56.5 | 36.3 |

Here are the key findings from our experiment:

- Annualized Returns: Across all rebalancing frequencies, our momentum strategy consistently delivered attractive annualized returns. However, the magnitude of returns varied depending on the rebalancing frequency employed.

- Volatility: Rebalancing frequency had a noticeable impact on portfolio volatility. Generally, more frequent rebalancing resulted in lower volatility, while less frequent rebalancing led to higher volatility.

- Max Drawdown: The maximum drawdown, representing the peak-to-trough decline in portfolio value, exhibited sensitivity to rebalancing frequency. Strategies with more frequent rebalancing tended to experience lower maximum drawdowns, indicating better downside protection.

Alternative Approaches to Rebalancing

Beyond traditional calendar-based rebalancing, alternative approaches can be considered:

- Threshold-based Rebalancing: Rebalance the portfolio when asset allocations deviate from predetermined thresholds. This approach offers flexibility and can help avoid unnecessary trades in stable market conditions.

- Volatility-based Rebalancing: Rebalance the portfolio based on changes in market volatility. When volatility exceeds a certain threshold, the portfolio is rebalanced to manage risk effectively. This approach is particularly useful in highly volatile markets.

Conclusion

Our experiment sheds light on the relationship between rebalancing frequency and the effectiveness of long-term relative momentum strategies in the Indian stock market. While all tested frequencies exhibited positive returns, the choice of rebalancing frequency influenced portfolio volatility, downside risk, and risk-adjusted performance.

Among the tested rebalancing frequencies, we observed that one month seems to the optimal horizon for rebalancing looking at risk adjusted returns. This suggests that monthly may be the preferred choice for investors seeking to optimize the performance of their momentum strategy.

Our experiment underscores the importance of a well-calibrated rebalancing strategy in navigating the dynamic landscape of momentum investing. By understanding the factors influencing rebalancing frequency and exploring alternative approaches, investors can optimize portfolio performance while effectively managing risk. Join us in embracing the art and science of rebalancing as we chart a course toward investment success in the world of momentum strategies.

Explore Wright Research smallcases here

Wryght Research & Capital Pvt Ltd•SEBI Registration No: INA100015717

103, Shagun Vatika Prag Narayan Road, Lucknow, UP 226001 IN

CIN: U67100UP2019PTC123244

Disclaimer: Investment in securities market are subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, membership of BASL and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors. The content in these posts/articles is for informational and educational purposes only and should not be construed as professional financial advice and nor to be construed as an offer to buy/sell or the solicitation of an offer to buy/sell any security or financial products. Users must make their own investment decisions based on their specific investment objective and financial position and use such independent advisors as they believe necessary.

You may want to read

Expert Analysis of the Global Macro Events & News affecting the Indian Markets

The Good Bad and Ugly weekly review : 4 July 2023

Interest Rate Cut Expectations In 2024 For India, US & the World: Impact On Stock Markets

Expert Analysis of the Global Macro Events & News affecting the Indian Markets

The Good Bad and Ugly weekly review : 4 July 2023

Interest Rate Cut Expectations In 2024 For India, US & the World: Impact On Stock Markets